The newest headlines from our reporters throughout the US despatched straight to your inbox every weekday

Your briefing on the newest headlines from throughout the US

Your briefing on the newest headlines from throughout the US

The IRS has unveiled new federal revenue tax brackets to account for inflation – with the hope of offering aid for some People once they file their taxes for subsequent yr.

Regardless of its partial closure because of the authorities shutdown, the company shared particulars Thursday of the brand new federal revenue tax brackets and customary deductions, which apply to tax yr 2026 for returns filed in 2027.

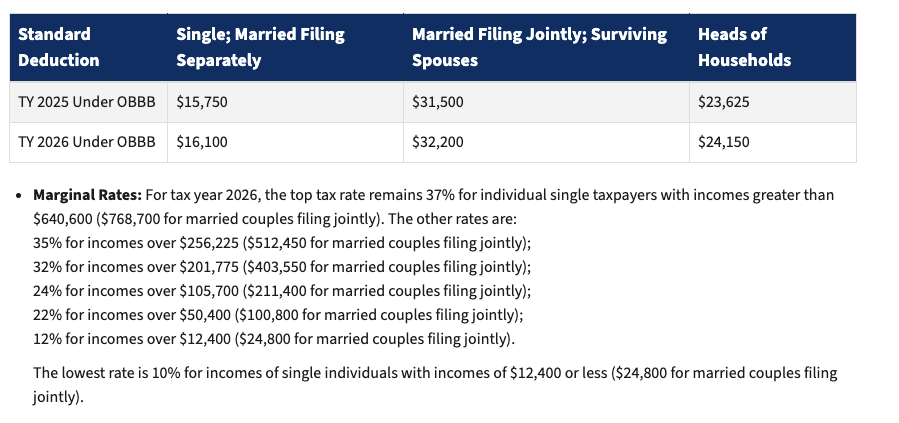

The IRS lets most filers decrease their taxable revenue by taking the usual deduction, which is a flat quantity primarily based on submitting standing and age, in accordance with NerdWallet.

For 2026, the usual deduction might be raised from $31,500 to $32,200 for married {couples} submitting collectively. For single taxpayers and married folks submitting individually, the usual deduction will improve from $15,750 to $16,100.

The IRS additionally shared adjustments to particular person revenue tax brackets. Whereas tax price percentages will keep the identical, because of Trump’s One Large Stunning Invoice that handed in July, the incomes threshold to enter a brand new tax bracket has been adjusted for inflation.

open picture in gallery

For 2026, the highest price of 37 % applies to people with taxable revenue above $640,600 and married {couples} submitting collectively incomes $768,700 or extra.

Elevating the incomes threshold may probably create financial savings for some People who haven’t acquired a pay increase to counteract the rising value of meals, housing, gasoline and different requirements.

The IRS makes changes annually, usually in October or November, to keep away from what is called “bracket creep,” which happens when inflation pushes folks into greater tax brackets, forcing them to pay extra come Tax Day.

A number of different adjustments past the federal tax brackets had been shared Thursday, together with adjustments to HSAs and FSAs.

Beginning subsequent yr, individuals who contribute to a well being versatile spending account (FSA) can contribute as much as $3,400 and, if their plan permits it, carry over as much as $680 into the following tax yr.

open picture in gallery

The 2026 contributions for well being financial savings accounts will improve to $4,400 for self protection and $8,750 for household protection.

The annual exclusion for items, which restricts how a lot taxpayers may give another person with out submitting a present tax return, might be $19,000 per individual for 2026, which is identical because it was in 2025.

Different adjustments embody a rise within the property tax credit score, which establishes a threshold for the taxation of estates upon a rich individual’s demise. In 2026, estates valued at or beneath $15 million won’t be topic to property tax, which is up from $13.9 million in 2025.

In the meantime, the earned revenue tax credit score, which was created to present a break to qualifying taxpayers with youngsters, may even improve from $8,046 to $8,321.

The IRS bulletins come a day after the company stated it might furlough almost half of its workforce because of the authorities shutdown, which has now entered its ninth day.

")

{kind=link}